Which tier will I use?

This information helps you decide which reporting tier to use and explains some important accounting terms.

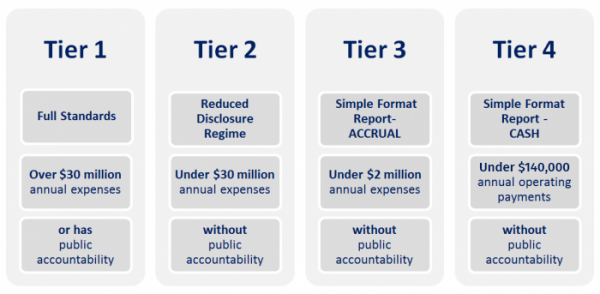

The reporting standards are part of a tiered system. All charities default into Tier 1, but may choose to report in another tier if they meet certain criteria.

The criteria for each tier are shown below. The tier that a charity reports under is determined by the annual expenses or operating payments of its previous two financial years. Look at your last two annual financial statements for this information.

Please note that the expense thresholds must be viewed in the context of the previous two financial periods. For example, if you had annual operating expenses of less than $140,000 in the financial years ended 31 March 2020 and 31 March 2021 you would be entitled to use Tier 4 regardless of whether your annual operating expenses for the year ended 31 March 2022 were above or below $140,000. If, on the other hand you had annual operating expenses greater than $140,000 for the years ended 31 March 2020 and 31 March 2021, but in the year ended 31 March 2022 you had annual operating expenses of less than $140,000, you would be required to use the Tier 3 standard because the threshold applies to the previous two periods, not the current period. The reason for this is to take into account any one-off fluctuations in expenditure that might otherwise require a charity to report under a higher tier.

Charities with annual expenses over $30 million, or with public accountability (see below), must report using Tier 1 standards. All other charities may choose to use a lower tier if they meet the criteria.

If you meet the criteria of two different tiers, refer to the information about ‘Moving between tiers.’

Public accountability

We expect that very few charities have public accountability, and those organisations that do will be aware of it. There are two quick questions to help you decide if you have public accountability:

Do people give you cash or assets that you hold for them?

This is typically the case for banks, credit unions, insurance providers, securities brokers/dealers, mutual funds and investment banks.

Is this one of your main activities?

If you answered yes to both of these questions, your charity may have public accountability and be required to report under Tier 1. Refer to the External Reporting Board (XRB) website(external link) for further information.

Expenses and operating payments

'Expenses' for the purposes of the standards are the expenses of an organisation’s day-to-day activities. Expenses do not include capital expenses, for example the purchase of fixed assets, adding to the value of an existing fixed asset, or the repayment of debt. A fixed asset is something of significant value to the organisation that lasts longer than 12 months. Some examples of expenses and capital expenses are shown in the table below.

Operating payments are expenses that have been paid for. Operating payments do not include accrual-based accounting concepts such as depreciation or money that you owe. The Tier 4 criteria are based on operating payments to reflect cash-based accounting.

Expenses |

Petrol Motor vehicle repair Insurance Rent Stationery Office supplies Printing Advertising Fundraising costs |

Grants/donations made Salaries and wages Legal fees Accounting fees Audit fees Travel expenses Training for staff Power Building maintenance and repairs |

Capital expenses |

Motor vehicles Land Buildings |

Computers Furniture Office equipment |

Cash-based accounting and accrual-based accounting

Under cash-based accounting, transactions are recorded at the time that cash is received or paid, rather than when earned or incurred. Cash-based accounting is typical in organisations where transactions tend to be small in number and size, and relatively uncomplicated. A cash book, which could be paper based or in an excel workbook, is usually used in cash-based accounting to record transactions.

Under accrual-based accounting, revenue and expenses are recorded when they are earned or incurred, rather than when cash is received or paid (for example, if your charity has had confirmation that it will receive a grant, but it has not yet been paid, you would still record this as revenue). Accrual-based accounting is typical in organisations with a significant number of transactions, recorded using accounting software, often with the help of an accountant. Accrual-based accounting allows for concepts such as depreciation and bad debts.

The main difference between cash and accrual accounting is the timing of when receipts/revenue (money coming into your charity) and payments/expenses (money paid out by your charity) are recorded.

What does this mean for me?

If you do not have public accountability, and you currently use cash-based accounting, and your operating payments are:

- under $140,000: you can choose to use Tier 4 which will allow you to continue using cash-based accounting.

- $140,000 or more: you will need to start using accrual-based accounting because you will report in Tier 1, 2 or 3.

If you do not have public accountability, you currently use accrual-based accounting, and your operating payments are:

- under $140,000: you may choose to use Tier 3 so that you can continue using accrual-based accounting. If you choose to use Tier 4, you will have to change to cash-based accounting.

- $140,000 or more: you will report in Tier 1, 2 or 3 where you can continue to use accrual-based accounting

Moving between tiers

Some charities’ annual expenses or operating payments may change so that they no longer qualify for the tier they have been using. Charities can continue to report in that tier for the current and following financial years. They do not need to report at the higher tier until they have had two consecutive financial years of annual expenses or operating payments above their current tier threshold.

Charities with expenses or operating payments that are around the threshold levels of the tiers, or that fluctuate between the threshold levels, or that know they will exceed the threshold in the future, may want to consider reporting at the higher tier to avoid having to change reporting tiers.

It is important to note that charities moving from Tier 4 to Tier 3 will need to change to accrual-based accounting.

More information

For more information about the criteria and requirements for moving from one tier to another, please refer to the XRB website(external link) and the standard: